Introduction

Many investors hold rail equities believing they understand M&A risk. They track antitrust precedent, monitor DOJ staffing, and model deal-close probabilities using standard event-driven frameworks. That playbook breaks completely when a Class I railroad merger hits the Surface Transportation Board.

The STB doesn't apply antitrust law in the way most investors expect. It applies a public interest standard — evaluating service reliability, shipper access, safety records, labor impacts, and infrastructure control alongside competitive effects. Standard M&A probability models are unreliable for rail deals because a merger can pass narrow competition tests while still failing on service commitments or gateway access.

That distinction is playing out now. Union Pacific's proposed $85 billion acquisition of Norfolk Southern — the largest proposed rail merger in decades — has already been rejected as incomplete by the STB. How this deal navigates regulatory review will define investment risk for anyone holding rail equities, shipper-adjacent stocks, or sector ETFs over the next several years.

TLDR

- STB review runs 15–18 months minimum post-acceptance, with no guarantee of unconditional approval.

- Approval weight covers safety, labor, service commitments, and infrastructure access — not just competition.

- The UP-NS application was rejected as incomplete in January 2026 over traffic modeling and gateway control deficiencies.

- Conditional approvals are the norm: divestitures, access mandates, and service benchmarks routinely cut projected upside.

Why Rail Merger Regulation Is Different From Other M&A

Most large corporate mergers are reviewed by the DOJ or FTC under antitrust standards focused on market concentration and consumer harm. Rail mergers involving Class I carriers fall under the Surface Transportation Board, which applies a broader "public interest" standard.

The STB evaluates:

- Whether the merger adds genuine competition or merely preserves existing market share

- Concrete service assurance mechanisms to compensate shippers for failures

- Routing changes, emissions exposure, and infrastructure footprint

- Historical safety performance, derailment records, and operational integration risk

- Workforce reduction, contract harmonization, and employee protections

A merger can clear a narrow antitrust screen and still fail STB review on service commitments or infrastructure access. STB Chairman Patrick Fuchs has stated the Board evaluates competitive effects, economic efficiencies, service effects, environmental impact, safety, and employee impacts. That's a substantially broader mandate than standard merger review — and one that standard M&A probability models aren't built to price.

The UP-NS Deal: What Investors Have at Stake

Union Pacific proposed acquiring Norfolk Southern in a transaction valued at approximately $85 billion, with per-share consideration of $320 (1.0 UP share plus $88.82 cash). The combined network would span over 50,000 route miles across 43 states, creating the first coast-to-coast railroad in the U.S. and connecting East, West, and Gulf Coast ports.

Primary Investor Thesis:

- Generates expected annualized synergies of approximately $2.75 billion through network consolidation

- Positions the combined carrier to convert long-haul truck freight to rail, unlocking new revenue streams

- Introduces Committed Gateway Pricing (CGP), letting BNSF and CSX quote end-to-end transcontinental rates at key interchange points (Chicago, St. Louis, Memphis, New Orleans) without separate UP/NS revenue agreements

Competing Risk Thesis:

- Concentrates an estimated 40% of all rail traffic under a single carrier — the American Chemistry Council and other major shipper groups argue this extends captive shipper exposure for chemical and agricultural freight

- Hands UP control over critical gateway infrastructure at St. Louis — including Mississippi River bridges and joint-use yards — prompting BNSF's public opposition and a formal statement from Canadian National

- Faces organized labor resistance from day one: the Transport Workers Union opposed the merger at announcement, and BLET and BMWED have formally opposed the deal on safety and cost grounds

Domino Risk for Investors:

Multiple analysts have warned that an approved UP-NS merger would likely prompt BNSF and CSX to pursue their own combination, reducing Class I railroads from six to four. For rail-adjacent investors, that means watching not just this deal's outcome, but whether approval triggers a second consolidation wave — one that would reprice competitive dynamics across intermodal, bulk, and manifest freight markets.

Union Pacific's Financial Position:

Union Pacific maintains a dividend track record with total 2025 dividends of $5.44 per share. Fitch Ratings placed Union Pacific on Rating Watch Positive following the merger announcement, though balance sheet flexibility could be constrained if deal costs, required divestitures, or concessions delay projected synergies.

The STB Review Process: Where Deals Stall and Why It Matters

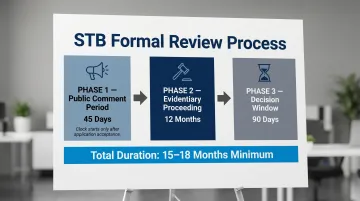

Formal Timeline Framework

Once an application is accepted as complete, the STB review process follows this timeline:

- 45-day public comment period opens

- Year-long evidentiary proceeding follows

- 90-day decision window after the evidentiary record closes

From acceptance to decision, investors should expect 15 to 18 months minimum, assuming no procedural delays.

But that clock doesn't start until the application is accepted.

The Sufficiency Challenge and Investment Implications

Before the formal review begins, the STB must determine whether the application is complete. On January 16, 2026, the STB unanimously rejected the UP-NS application as incomplete, citing:

- Lack of forward-looking market share impact analyses

- Missing exhibits and schedules, including Schedule 5.8 describing "materially burdensome regulatory condition" walk-away terms

- Misclassification of a related Terminal Railroad Association of St. Louis (TRRA) application as "minor" rather than "significant"

When the STB requests resubmission, the entire timeline resets. Investors holding positions based on estimated deal-close dates face indeterminate delays.

Three Areas Where STB Historically Requires More Detail

The Board's evidentiary standards are demanding in three recurring areas:

- Competitive Enhancements: The STB expects concrete evidence of new routing options, new shipper choices, or new service capabilities — not just assurances that existing competition will be preserved.

- Service Assurance: Vague commitments to "maintain service levels" are insufficient. The STB requires enforceable benchmarks and concrete mechanisms to compensate shippers for service failures.

- Infrastructure Access: Shared gateway cities — St. Louis, Chicago, and New Orleans — receive particular scrutiny. The Board's January decision flagged the TRRA issue as requiring "significant" transaction review, signaling sensitivity to gateway control.

Role of Outside Parties in Extending the Review

These documentation gaps don't just delay the clock — they open the door wider for intervention. Class I competitors (CSX, BNSF), shipper coalitions, state attorneys general, and federal labor organizations all have standing to submit evidence, challenge applicant claims, and present alternative models. Each intervention adds complexity and can influence both the timeline and any final conditions.

What Conditional Approval Means for Investors

The STB can approve a merger while mandating:

- Divestitures of specific routes or terminals

- Open access to competitors on specific routes

- Service performance benchmarks with penalties for failure

- Pricing oversight or rate caps

These conditions can erode the synergy estimates and pricing power investors priced into the original deal thesis.

Four Regulatory Risk Factors Investors Must Track Right Now

Five Regulatory Risk Factors Investors Must Track Right Now

Application Completeness and Resubmission Risk

The STB's January 2026 rejection of the UP-NS filing is not a minor procedural issue. The Board identified material deficiencies in traffic flow modeling and competitive harm analysis. Until the applicants refile and the STB accepts the application as complete, investors face an indeterminate delay before the formal review clock starts.

Actionable tracking: Monitor STB Docket No. FD 36873 for any formal requests for supplemental information or applicant resubmission filings. The applicants were directed to file by February 17, 2026, indicating whether they intend to refile.

Gateway Control and Structural Access Risk

The STB's decision to reclassify the TRRA filing as a "significant" transaction signals Board sensitivity to gateway control issues in St. Louis. If UP-NS is forced to divest gateway assets or grant open-access rights to competing carriers, the network efficiency assumptions underlying the deal's financial projections could be materially altered.

Actionable tracking: Watch how UP-NS addresses St. Louis gateway control in any revised filing. Forced divestiture or access mandates change the operational synergy math.

Safety Record and Labor Opposition as Regulatory Weight

The STB public interest standard explicitly considers safety. Major rail unions have formally opposed the merger, and Norfolk Southern's operational strides since the February 2023 East Palestine derailment remain fresh in the regulatory record.

Actionable tracking: Evaluate whether the STB incorporates safety testimony and labor opposition into the evidentiary record, and how past mergers have handled similar opposition.

Political and Antitrust Environment Shift

President Trump stated the proposed merger "sounds good to me" and praised Union Pacific, signaling a potentially more permissive posture. However, state attorneys general and competing railroads are independently challenging the application.

Watch for: Whether STB personnel changes represent a genuine regulatory shift or a surface-level reshuffling with no policy consequence. Track any congressional commentary on rail consolidation.

Cascading Industry Consolidation Signal Risk

Regardless of the UP-NS outcome, the merger announcement has already prompted rival railroads to signal potential defensive responses. The STB has stated concern about reducing Class I railroads below the current six — a ceiling that shapes how any second consolidation wave gets reviewed.

Investors holding BNSF parent (Berkshire Hathaway), CSX, or Canadian National should evaluate whether follow-on consolidation would be accretive or dilutive given current debt levels and that structural constraint.

To track: Monitor public statements from Class I railroad CEOs and any informal STB guidance on industry structure. A defensive merger announcement from a rival carrier would accelerate the timeline on these questions.

Each of these five risk factors can move independently — a safety ruling doesn't wait for the antitrust review, and political signals don't bind the Board. Investors who track them separately, rather than as a single regulatory outcome, will have more decision points and more time to act.

Historical Precedent: Lessons From Past Rail Mergers

The CP-KCS Merger (2023)

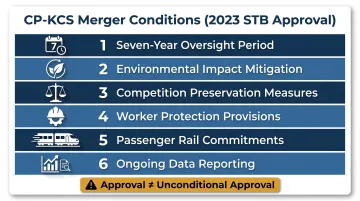

The most recent major rail merger was Canadian Pacific's acquisition of Kansas City Southern, approved by the STB on March 15, 2023, effective April 14, 2023, creating CPKC.

Conditions imposed:

- Seven-year oversight period — longer than any prior STB approval

- Environmental impact mitigation requirements tied to specific corridors

- Competition preservation measures protecting shippers on overlapping routes

- Worker protection provisions covering labor displacement

- Passenger rail promotion commitments along shared lines

- Ongoing data reporting obligations to the STB throughout the oversight window

The STB's willingness to impose long-term oversight and multiple conditions demonstrates that approval does not mean unconditional approval. Investors evaluating any proposed Class I merger should use CP-KCS as a calibration point — not just for timeline expectations, but for the operational and financial drag that conditions can impose post-close.

Broader Structural Lesson

CP-KCS is one data point in a longer consolidation arc. Since the Staggers Rail Act, the number of Class I railroads has declined from dozens in 1980 to six today. The historical record consistently shows the STB favors conditional approval over outright rejection — but the conditions matter as much as the approval itself.

A merger that closes under a seven-year oversight regime with mandated divestitures and reporting obligations is a materially different investment than the deal announced on day one.

How Boards and Investors Should Frame Oversight of M&A Regulatory Risk

Prolonged regulatory proceedings require a different governance posture than typical deal-close timelines. Boards and investment committees overseeing positions in companies undergoing major STB review need clear decision rights, defined escalation thresholds, and scheduled re-evaluation points — rather than a "wait and see" posture that lets uncertainty accumulate without structured response.

When risk is visible and evolving, the discipline is in structured monitoring — not reactive response. The frameworks that hold up under real regulatory pressure are the ones where decision authority is defined before the headlines arrive, escalation thresholds are set in advance, and reporting is built to drive decisions, not generate noise.

Three Signals That Should Trigger Board-Level Re-Evaluation:

- A formal STB request for application resubmission, which signals material deficiencies and effectively resets the timeline

- Conditional approval with divestitures or pricing mandates that differ materially from the original deal terms

- A second consolidation move by BNSF or CSX that shifts the competitive landscape assumptions underlying the original thesis

Three Practical Monitoring Disciplines During Extended Regulatory Review:

- Track the STB public docket directly rather than relying solely on company press releases. Regulatory filings surface adversarial positions and Board concerns well before they appear in management commentary.

- Evaluate management's quarterly commentary for language changes around synergy confidence or deal timeline — shifts in tone or specificity signal internal reassessment.

- Assess balance sheet resilience — whether dividend coverage and debt service capacity hold up if the review extends beyond 18 months without resolution.

Frequently Asked Questions

How long does the STB review process typically take for a major rail merger?

The STB's formal timeline runs about 15 to 18 months: a 45-day comment period, a year-long evidentiary proceeding, and a 90-day decision window. Pre-acceptance challenges on application completeness can push the total well beyond that baseline, as the UP-NS rejection in January 2026 demonstrated.

Can the STB block a major rail merger outright?

Yes, the STB has authority to deny applications, but historically it has been more likely to impose conditions than issue outright rejections. Conditions such as divestitures, open access mandates, or service performance benchmarks can materially alter the financial case for a merger, even if the deal is technically "approved."

What conditions has the STB imposed on past rail mergers?

Typical conditions include competitive access requirements, shipper service guarantees with penalty provisions, infrastructure divestitures in shared gateway markets, and labor protections. The 2023 CP-KCS approval added a seven-year oversight period covering environmental, competitive, and worker protections.

How does the UP-NS merger differ from the 2023 CP-KCS merger that created CPKC?

The UP-NS deal would be a domestic end-to-end combination rather than a cross-border merger, it would reduce domestic Class I carriers from six to five, and the scale of potential competitive impact on shared domestic gateways (St. Louis, Chicago, New Orleans) is larger than anything CP-KCS posed.

What does "captive shipper" risk mean for investors, and why does it matter in this merger?

Captive shippers are facilities served by only one railroad with no competitive alternative. Critics argue the UP-NS merger extends captive exposure for chemical, agricultural, and industrial shippers, concentrating market power. This matters to investors because pricing power concentration can invite future regulatory rate oversight or shipper legislation that limits revenue upside.

What should investors monitor in UP and NSC stock during the STB review period?

Four indicators matter most during the review period:

- STB docket activity for application status and procedural rulings

- Management guidance on deal timelines and synergy confidence

- Balance sheet metrics including dividend coverage and debt service capacity

- Competitor announcements signaling a second consolidation wave

Any of these shifting negatively should prompt a reassessment of deal probability and timeline.