Board member liability insurance, commonly called Directors and Officers (D&O) insurance, exists to close this gap. This guide covers what D&O insurance is, what it covers, who needs it, what it costs, and how strong governance practices reduce exposure before claims ever arise.

TLDR

- D&O insurance protects board members' personal assets from claims alleging wrongful acts in their governance role

- Coverage extends to for-profit, nonprofit, and private companies—not just public corporations

- Policies cover defense costs (often $10 million or more), settlements, and regulatory investigations

- Fraud, criminal acts, and intentional misconduct are excluded, but defense costs are covered until a final ruling

- Strong governance documentation reduces claim frequency and strengthens defensibility

What Is Board Member Liability Insurance?

Board member liability insurance—also known as Directors and Officers (D&O) insurance or management liability insurance—protects individuals serving in board or executive roles from personal financial loss when sued for alleged wrongful acts performed in their leadership capacity. Unlike general liability insurance that shields the company as an entity, D&O insurance specifically protects the personal assets of individual board members.

The Three Coverage Sides

D&O policies operate through three distinct coverage layers:

| Coverage Side | Who It Protects | When It Applies |

|---|---|---|

| Side A | Individual directors and officers | When the company cannot or will not indemnify — bankruptcy, insolvency, or disputed obligations |

| Side B | The company | When the company indemnifies a director or officer and seeks reimbursement from the insurer |

| Side C | The company entity | Securities-related claims, such as shareholder lawsuits alleging fraud or misrepresentation |

Side A is where personal asset exposure is highest. According to Lockton's analysis, when companies collapse into Chapter 7 liquidation, non-indemnifiable defense costs can reach into the millions — and Side A is the only coverage standing between directors and those bills.

Side B reimburses the company after it steps in to cover a director or officer. The company pays costs upfront, and the insurer reimburses the organization, protecting its balance sheet when fulfilling indemnification obligations.

Side C extends to the company itself for securities-related claims. While most relevant to publicly traded companies, this coverage increasingly appears in private company policies.

The Relationship Between D&O Insurance and Indemnification

Most companies have both indemnification agreements and D&O insurance. Indemnification is the company's contractual promise to protect its leaders; D&O insurance is the financial backstop that pays when the company cannot fulfill that promise. Board members should insist on seeing both before accepting a seat.

What D&O Insurance Covers—and What It Doesn't

Primary Covered Expenses

D&O policies cover three main cost categories:

- Legal defense costs: Attorney fees, court costs, and investigation expenses

- Settlements: Monetary agreements reached before or during trial

- Court-ordered judgments: Final rulings requiring payment to claimants

Defense costs alone frequently reach six or seven figures. Allianz Commercial reports that average legal defense costs for securities class actions reach approximately $10 million, with large cases reaching $100 million. Defense costs typically absorb 25%-33% of the total insured sum.

Settlement costs have also reached historic highs. Cornerstone Research found the median securities class action settlement reached $17.3 million in 2025—a nearly three-decade high.

Employment-Related Claims Coverage

D&O policies cover employment-related claims involving board decisions:

- Wrongful termination decisions

- Workplace discrimination allegations

- Harassment claims tied to leadership conduct

- Failure to enforce company policy

Employment claims are especially frequent in smaller organizations without dedicated HR or legal teams—and they're often the first D&O claim a board encounters.

Regulatory Investigation Coverage

Many D&O policies extend beyond civil lawsuits to cover formal regulatory and government investigations. Key distinctions to understand:

- Investigative defense costs are typically covered

- Regulatory fines and penalties themselves are usually excluded

- Civil and criminal investigations can run simultaneously, creating parallel cost exposure

What Is NOT Covered

Understanding what D&O covers is only half the picture. Standard exclusions include:

- Fraudulent or dishonest acts

- Criminal activity

- Intentional violations of law

- Illegal personal profits

- Bodily injury or property damage (covered under other policies)

Most policies include a "conduct exclusion" that only activates after a final adjudication of fraud. According to ABA Business Law analysis, defense costs are typically still covered during investigation and trial phases—even if the outcome is ultimately unfavorable.

The InterMune v. Harkonen case illustrates this: a former CEO convicted of felony wire fraud received advanced defense costs throughout years of litigation, but was ordered to repay approximately $6 million after exhausting all appeals.

Cybersecurity Governance Claims: A Growing Risk

Boards are increasingly named in lawsuits following major data breaches or technology failures, with claimants alleging the board failed in its oversight responsibilities.

Real-world example: Following the SolarWinds cyberattack, investors sued directors in a derivative suit alleging they knew about and failed to monitor cybersecurity risks. Separately, the SEC charged the company and its CISO personally regarding cybersecurity practices and disclosures.

In October 2024, the SEC charged four companies (Unisys, Avaya, Check Point, Mimecast) with civil penalties ranging from $990,000 to $4 million for misleading disclosures about the SolarWinds Orion hack—downplaying actual incidents as hypothetical risks.

For boards reviewing their D&O coverage, this is a practical question: does your policy specifically address cyber oversight failures, or does it leave a gap that regulators are now actively exploiting?

Why Board Members Face Personal Liability

Breach of Fiduciary Duty

The most common claim basis against board members is breach of fiduciary duty. Board members owe three core duties:

- Duty of care: Making informed, deliberate decisions before acting

- Duty of loyalty: Prioritizing the organization's interests over personal gain

- Duty of obedience: Adhering to the organization's mission and applicable legal obligations (in some jurisdictions)

Breach allegations stem from financial decisions that led to losses, conflicts of interest, related-party transactions, or failure to implement adequate oversight systems.

Regulatory and Government Enforcement

Regulatory bodies across financial services, healthcare, environmental compliance, and data protection can target board members directly when they find the board enabled or ignored violations.

The SEC alone brought 583 enforcement proceedings in 2024, with individual-level actions that included:

- An NYSE-listed company director fined $175,000 plus a five-year officer/director bar for failing to disclose a personal relationship

- 23 officers, directors, and major shareholders charged in a single action for beneficial ownership reporting violations

Shareholder and Investor Claims

Disgruntled shareholders may sue board members if they believe leadership misrepresented company financials, made decisions that eroded share value, or failed to disclose material information. Even board members who voted against a specific decision can be named simply because they held a seat.

Research published in the Journal of Financial Economics found that approximately 11% of independent directors were named as defendants in securities class action lawsuits from 1996 to 2010.

Cyber Oversight Liability: The Emerging Vector

Boards that cannot demonstrate they asked the right questions about cybersecurity risk, reviewed appropriate metrics, or ensured adequate controls may face personal exposure following major incidents.

Delaware law established the Caremark standard: a board's "utter failure to attempt to assure a reasonable information and reporting system exists" constitutes bad faith and breach of the duty of loyalty. In Marchand v. Barnhill (Delaware Supreme Court, 2019), the court ruled that failure to implement any system to monitor "mission critical" compliance issues supports an inference of bad faith.

These precedents make the standard clear: boards are accountable for governance failures that allowed a breach environment to exist, not only for the breach itself.

Who Needs Board Member Liability Insurance?

Private Companies, Startups, and Nonprofits Are Just as Exposed

D&O insurance isn't a large public company problem. Private companies, startups, and small businesses face the same claim types — and have far fewer internal resources to absorb them.

Allianz's 2026 D&O Insights report confirms that private company D&O claims are primarily driven by bankruptcy and regulatory enforcement actions. Global business insolvencies are projected to rise 6% in 2025 and 5% in 2026, reaching 24% above pre-pandemic averages.

Nonprofit Board Members Are Exposed Too

Nonprofit status does not eliminate personal liability. Nonprofit board members can be sued for:

- Misuse of charitable funds

- Breach of fiduciary duty

- Employment-related claims

- Regulatory violations

Some states offer limited volunteer protection statutes, but these have significant exceptions. The federal Volunteer Protection Act of 1997 has critical gaps. According to ASAE/Aon:

- Does not prevent volunteers from being sued—only limits liability if specific conditions are met

- Does not cover willful, criminal, reckless misconduct, or gross negligence

- Does not protect compensated directors or officers

- Does not cover legal defense costs

Nonprofit bankruptcy reached a 14-year high in 2024, increasing personal asset risk for directors and officers.

D&O Coverage Affects Board Composition and Investment

Organizations without D&O coverage often struggle to recruit qualified independent directors. Qualified candidates evaluate liability exposure before accepting board seats — and no coverage means higher personal risk.

The stakes are equally clear for investors. Berkley Select confirms that private equity and venture capital firms now require D&O insurance as a condition of investment. Woodruff Sawyer's 2026 GPL report found that for VC firms, D&O liability has overtaken outside directorship liability as the leading source of claims.

How to Evaluate and Choose a D&O Policy

Key Parameters to Assess

Coverage Limits

Evaluate both aggregate and per-claim limits. Early-stage companies may be limited to $1 million to $5 million in coverage, while limits of at least $10 million are often used to attract independent directors.

Retentions (Deductibles)

Know the retention amount the company absorbs before coverage kicks in — and whether that threshold changes for individual directors versus the entity.

Separated Side A Coverage

Verify that personal protection for individual directors (Side A) is not eroded by company-level claims (Sides B and C).

Defense Cost Treatment

Most D&O policies feature "shrinking limits"—defense costs are paid from within the policy limit, reducing the amount available for settlements. Given that defense costs can absorb 25%-33% of coverage, this erosion effect is critical.

Critical Exclusions to Review

Fraud Carve-Outs and Timing

Understand when fraud exclusions apply and whether defense costs are covered until a final ruling.

Prior Acts Coverage

Verify whether claims based on decisions made before the policy inception date are covered.

Claims-Made vs. Occurrence Triggers

D&O insurance is typically written on a claims-made basis, meaning the policy must be in effect both when the alleged wrongful act occurred and when the claim is made. This creates the need for retroactive date management and tail coverage.

Once you've mapped the exclusions that matter most, the next step is finding a broker who can translate those priorities into policy terms.

Work with a Specialist Broker

D&O pricing and coverage terms vary considerably based on:

- Industry (regulated sectors cost more)

- Company stage (pre-revenue vs. profitable)

- Governance quality

- Claims history

Underwriters now assess governance maturity as part of the underwriting process, including whether the board documents cyber oversight decisions.

Boards that maintain clear decision rights and demonstrate informed oversight tend to secure better premiums and terms — a direct return on governance discipline.

How Strong Board Governance Reduces Your D&O Exposure

D&O insurance pays after a claim is filed. The quality of a board's governance practices determines both how often claims arise and how defensible the board's position is once a claim is made.

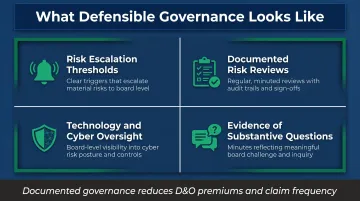

What Defensible Governance Looks Like

Boards that document their deliberations, maintain clear decision rights, and demonstrate informed oversight are far better positioned in legal or regulatory proceedings.

Delaware's Caremark/Marchand standards require board records showing evidence of consideration and deliberation:

- Specific agenda items addressing key risks

- References to management reporting in board minutes

- Written board materials

- Disclosure of material risks

Beyond documentation, defensible governance requires:

- Clear escalation thresholds for material risks

- Documented board-level risk reviews

- Consistent oversight of management reporting (especially on technology and cyber risk)

- Evidence that the board asked substantive questions and received credible answers

Governance Documentation Reduces Premiums

This documentation is now routinely reviewed during D&O underwriting—governance quality can directly affect both premiums and coverage terms. Allianz's 2026 report reinforces this: detailed records of key decisions are critical for defending against mismanagement claims and conflicts of interest, particularly during insolvencies.

The Role of Specialized Advisors

Boards bringing in specialized advisors—for cybersecurity oversight, technology risk, or governance structure—build the documented decision-making record that protects individual board members.

Tyson Martin works with boards on exactly this: establishing decision rights, documented risk thresholds, and oversight structures that hold up under regulatory scrutiny. That work reduces both the likelihood of a D&O claim and the cost of defending one if it arrives.

Frequently Asked Questions

Do board members need liability insurance?

Yes. Any individual serving on a board can be personally sued for alleged wrongful acts in their governance role, regardless of whether they acted in good faith. Without D&O insurance, legal defense costs alone—often reaching $10 million or more—can threaten personal assets including savings, homes, and retirement accounts.

Can nonprofit board members be held personally liable?

Nonprofit status does not eliminate personal liability. Volunteer protection statutes vary by state, carry significant exceptions, and cover nothing toward legal defense costs. D&O insurance remains essential for protecting board members' personal assets from claims alleging breach of fiduciary duty, misuse of funds, or regulatory violations.

What can directors be personally liable for?

Directors face personal exposure across a wide range of governance failures, including:

- Breach of fiduciary duty (care, loyalty, obedience)

- Financial mismanagement or regulatory violations

- Misrepresentation to investors or stakeholders

- Employment-related decisions

- Failures in technology and cyber oversight

Even directors who voted against a decision can be named in a lawsuit simply for holding a board seat.

What's the difference between E&O and D&O?

Errors and Omissions (E&O) insurance covers the company's liability for professional mistakes in services delivered to clients, while D&O insurance covers the personal liability of directors and officers for management and governance decisions. They protect different parties and different claim types—many organizations need both.

Is D&O insurance worth the cost?

For most organizations with a formal board, yes. The cost of D&O insurance is typically modest compared to the potential six- or seven-figure cost of defending a single lawsuit. Investors routinely require it, and coverage cannot be added retroactively once a claim is filed.

How much is directors and officers insurance for a nonprofit?

Nonprofit D&O premiums vary based on organizational size, budget, employee count, and claims history. Most nonprofits are seeing flat renewals or modest single-digit decreases in 2025 due to carrier competition. High-risk sectors—child welfare, affordable housing, higher education, and healthcare—are an exception, with some facing double-digit increases.